New EU Payment Rules Could Expand Fraud Monitoring: What Businesses Must Know

The European Union is tightening the screws on payment fraud. With the EU Instant Payments Regulation now in force and the Financial Supervisory Authority (FIN-FSA) actively reviewing bank compliance, organizations across the continent face a new era of expanded fraud monitoring. The rules, which entered into force in 2025, require payment service providers to implement real-time screening of transactions, share fraud data among institutions, and significantly enhance customer verification processes. For banks, fintechs, and merchants operating in the EU, these changes represent both a compliance challenge and a strategic opportunity to build trust in digital payments.

In this comprehensive guide, we break down what the new EU payment rules entail, who they impact, how they expand fraud monitoring, and what steps your organization should take to prepare. We also explore the broader implications for the payments ecosystem and provide actionable recommendations for staying ahead of regulatory expectations.

Key Changes Under the Regulation

- Real-time transaction screening: All instant payments must be screened for fraud and money laundering before being executed, with verification completed within seconds.

- Enhanced customer due diligence: PSPs must verify payer and payee identities for every instant transaction, even for low-value payments.

- Data sharing obligations: Institutions must now share fraud-related data with each other through centralized platforms, enabling faster identification of emerging threats.

- Liability shifts: In cases of unauthorized transactions, the burden of proof shifts to the PSP, making robust monitoring systems a legal necessity.

These changes represent a fundamental shift from the previous batch-processing model, where fraud checks could occur hours after a transaction was initiated. Now, every payment must be vetted in real-time, requiring significant technological upgrades.

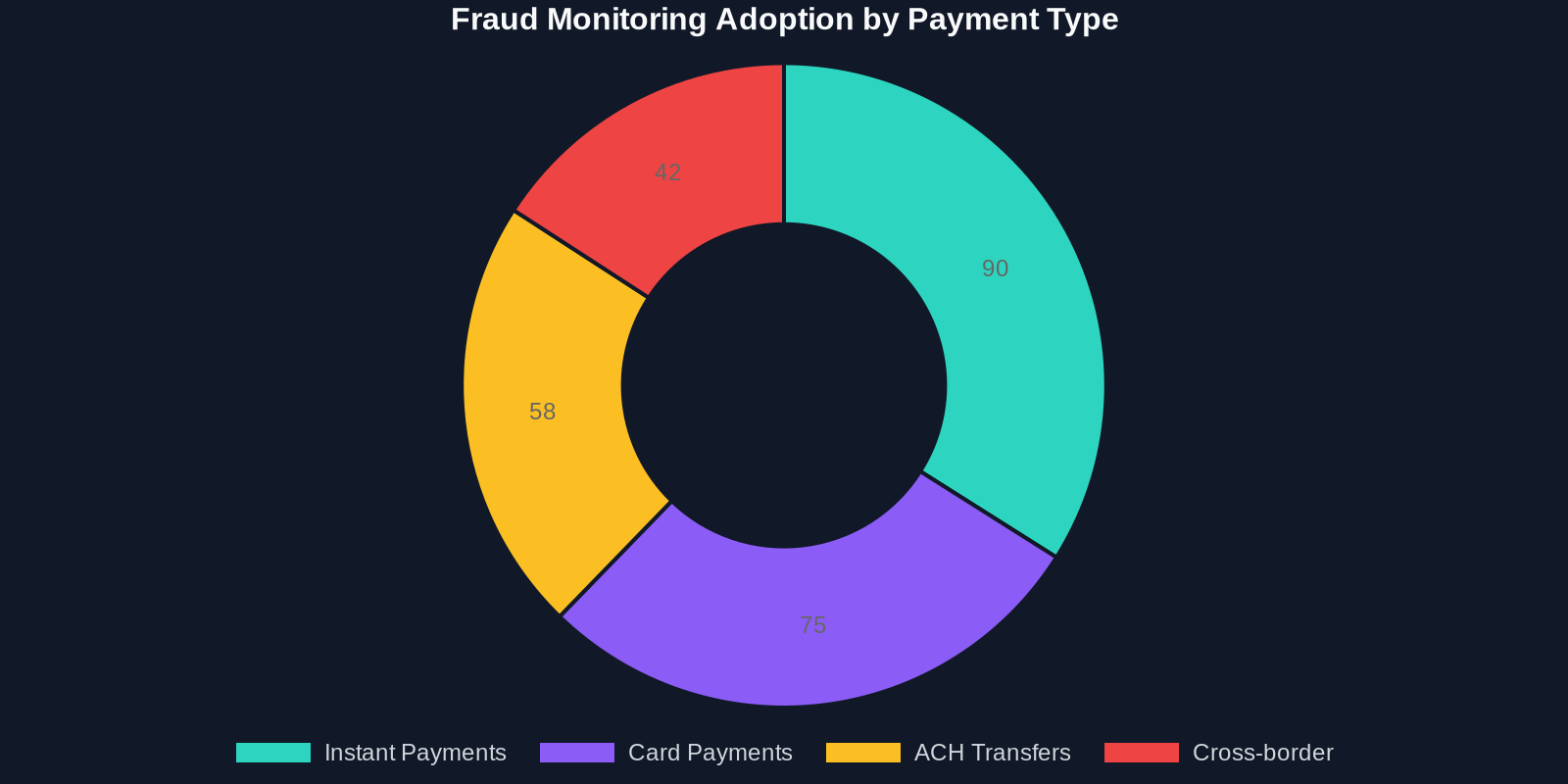

How Fraud Monitoring Is Expanding

Fraud monitoring under the new rules goes far beyond traditional transaction monitoring. The regulation explicitly requires PSPs to detect and prevent new forms of digital fraud, including authorized push payment (APP) scams, account takeover, and synthetic identity fraud.

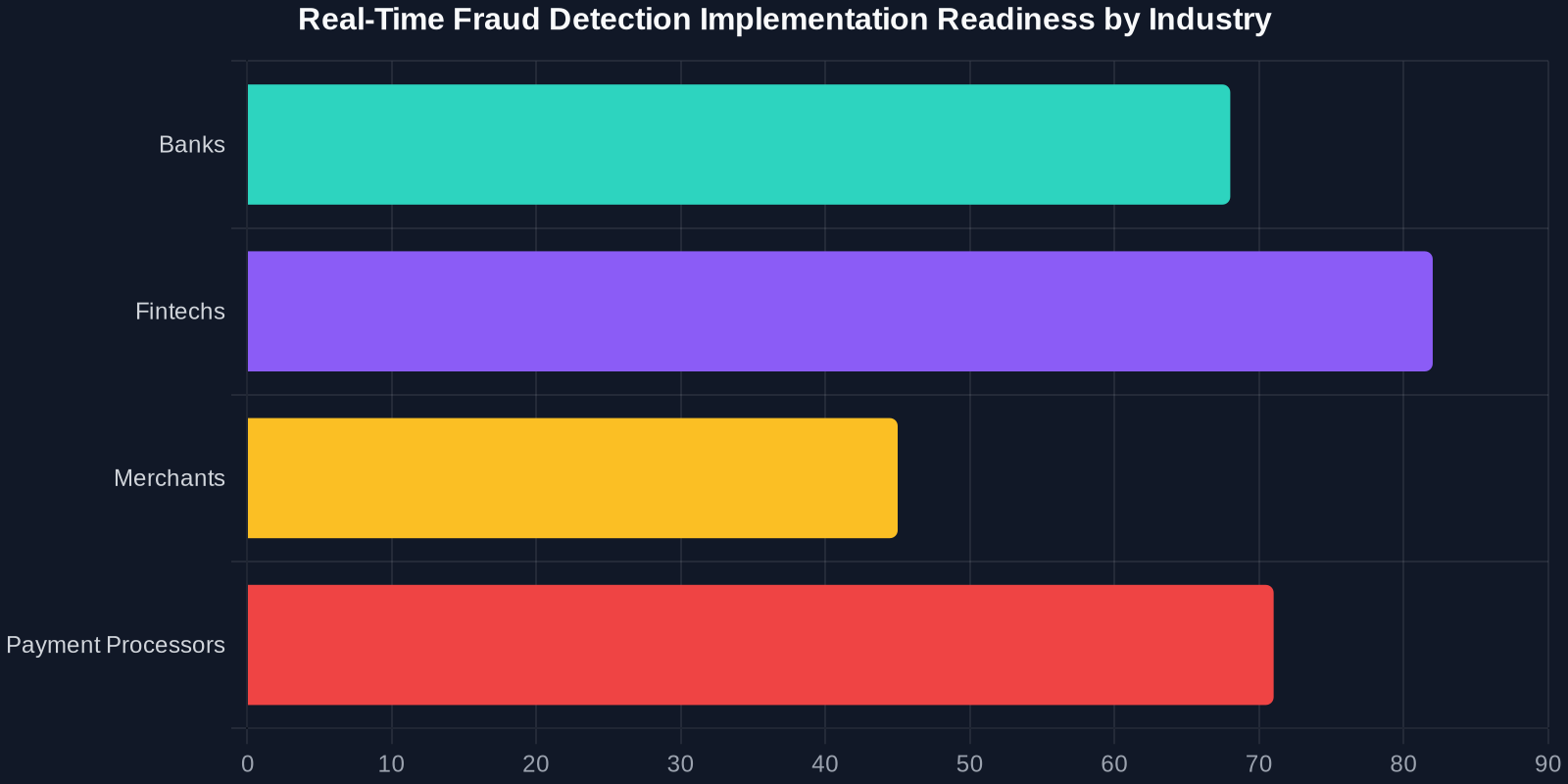

Banks and Traditional Financial Institutions

For established banks, the challenge is modernizing legacy systems. Many institutions still operate on mainframe-based payment processing that was never designed for real-time screening. Upgrading these systems requires significant capital investment and organizational change. However, the FIN-FSA has indicated that it expects full compliance from all licensed credit institutions by mid-2025.

Fintechs and Payment Service Providers

Digital-native fintechs may have an advantage in terms of technology, but they face unique compliance challenges. Many operate across multiple EU jurisdictions, each with its own interpretation of the regulation. The obligation to share fraud data also raises privacy concerns, as platforms must balance transparency with customer data protection under GDPR.

Merchants and E-commerce Platforms

Merchants are indirectly impacted through their payment service providers. As PSPs tighten fraud monitoring, merchants may experience higher decline rates for legitimate transactions, particularly for cross-border payments. Additionally, the cost of compliance may be passed down, leading to higher transaction fees.

Step 4: Train Your Team

Fraud monitoring under the new rules requires specialized skills. Ensure your compliance, risk, and technology teams are trained in:

- Real-time transaction monitoring techniques

- Data privacy regulations (GDPR) as they apply to fraud data sharing

- The specific requirements of the EU Instant Payments Regulation

- Incident response procedures for fraud events

The Broader Impact on the Payments Ecosystem

The new rules are not occurring in a vacuum. They are part of a broader global trend toward enhanced payment security and transparency.

Data Sharing and Privacy Trade-offs

One of the most debated aspects of the new rules is the mandatory sharing of fraud data. While this helps institutions identify emerging threats faster, it raises concerns about data privacy. PSPs must ensure that any data shared is anonymized and used solely for fraud prevention purposes.

Innovation Opportunities

The compliance requirements are also driving innovation. Many fintechs are developing new solutions specifically for real-time fraud detection, including:

- AI-based behavioral analytics that detect anomalies in user behavior

- Biometric authentication systems that verify identity without passwords

- Blockchain-based audit trails for transaction transparency

- Open banking APIs that enable richer data for risk scoring

Industry Reactions and Best Practices

Industry reaction to the new rules has been mixed. While many recognize the need for stronger fraud monitoring, some have expressed concerns about implementation costs and potential false positives that could block legitimate transactions.

As the FIN-FSA continues its review of bank compliance and as regulators across the EU harmonize their enforcement approaches, now is the time to act. Whether you are a bank processing millions of transactions daily or a fintech startup offering the latest payment innovation, the message is clear: fraud monitoring is no longer a back-office function—it is a core strategic priority.

Key Takeaways

The path to compliance is demanding, but the rewards—secure payments, customer trust, and regulatory confidence—are well worth the effort. Start your compliance journey today.